What is Whole Life Insurance and How Does It Work?

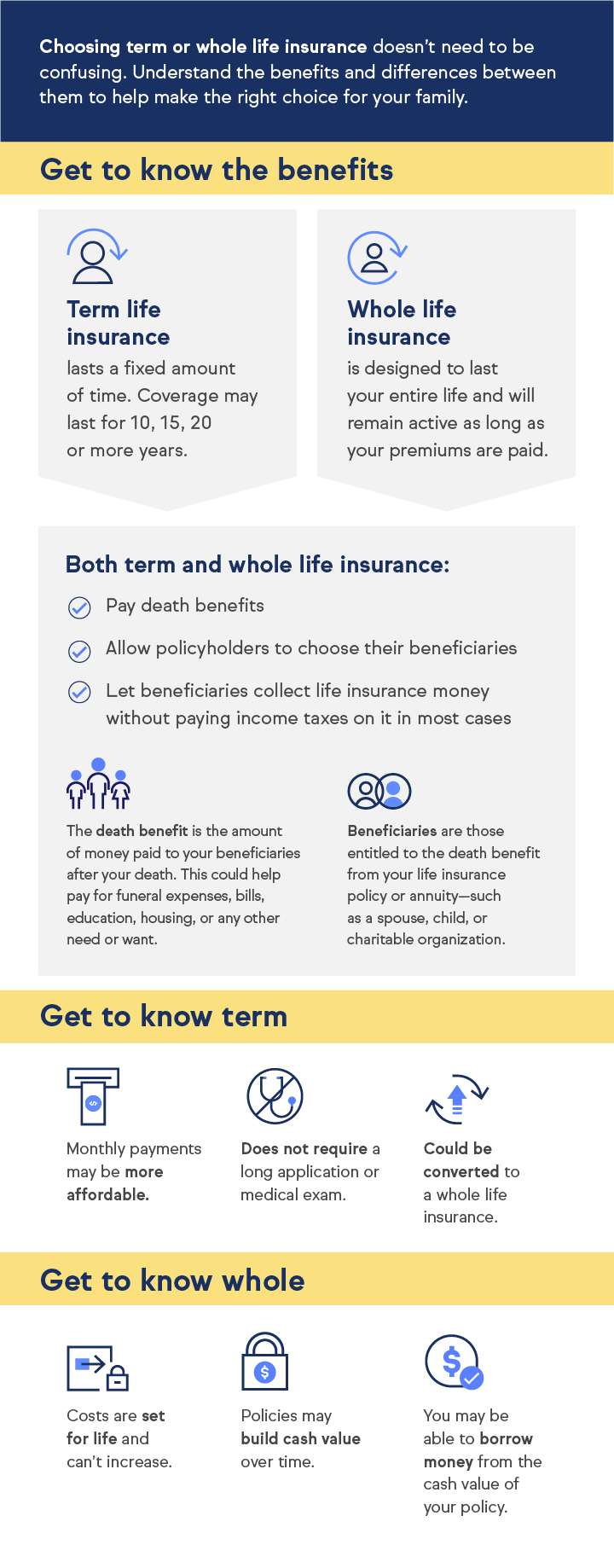

Whole life insurance is a type of permanent life insurance that provides coverage for the insured's entire lifetime, as long as premiums are paid. Unlike term life insurance, which lasts for a specific period, whole life policies accumulate cash value over time. This cash value, which grows at a guaranteed rate, can be borrowed against or even withdrawn if needed. This dual benefit of providing a death benefit and a savings component makes whole life insurance an appealing choice for those looking for long-term financial stability.

The mechanics of how whole life insurance works can be broken down into several key components:

- Premiums: Policyholders pay fixed premiums, which remain consistent throughout the life of the policy.

- Cash Value: A portion of the premium contributes to the policy’s cash value, which grows over time, typically at a rate specified by the insurer.

- Death Benefit: Upon the death of the insured, a death benefit is paid to the beneficiaries, which is usually tax-free.

The Benefits of Choosing Whole Life Insurance: A Comprehensive Guide

Whole life insurance provides a unique blend of benefits that make it a compelling choice for individuals looking to secure their financial future. Unlike term life insurance, whole life policies offer lifelong coverage, ensuring that your loved ones are protected no matter when you pass away. This permanence brings peace of mind, allowing you to focus on other aspects of financial planning. Moreover, whole life insurance accumulates cash value over time, which can serve as an important financial resource for emergencies, investments, or retirement funding.

In addition to lifelong coverage and cash value accumulation, whole life insurance offers predictable premiums. This means that the amount you pay remains constant throughout the life of the policy, making budgeting easier. Additionally, the growth of the cash value is typically tax-deferred, providing another layer of financial benefit. Many policyholders appreciate the ability to borrow against the cash value, providing them with liquidity without the need for a credit check. Overall, choosing whole life insurance can be an excellent strategy for comprehensive financial planning.

Is Whole Life Insurance Right for You? Key Questions to Consider

Deciding whether whole life insurance is right for you involves careful consideration of your financial goals, family needs, and personal values. Unlike term life insurance, which provides coverage for a specified period, whole life insurance offers lifelong protection and a cash value component that grows over time. Before making a decision, ask yourself the following questions:

- What are my long-term financial objectives?

- Do I need lifelong coverage to support my dependents?

- Am I comfortable with higher premium payments for a guaranteed death benefit?

Another important factor to think about is how whole life insurance fits into your overall financial strategy. Whole life policies can act as a savings vehicle, allowing you to borrow against the cash value or withdraw funds as necessary. However, the costs associated with these policies can be significantly higher than those of term life insurance. Consider these points before committing:

- Do I have other savings and investment options?

- How will the premiums impact my cash flow?

- Am I prepared for the long-term commitment that whole life insurance requires?