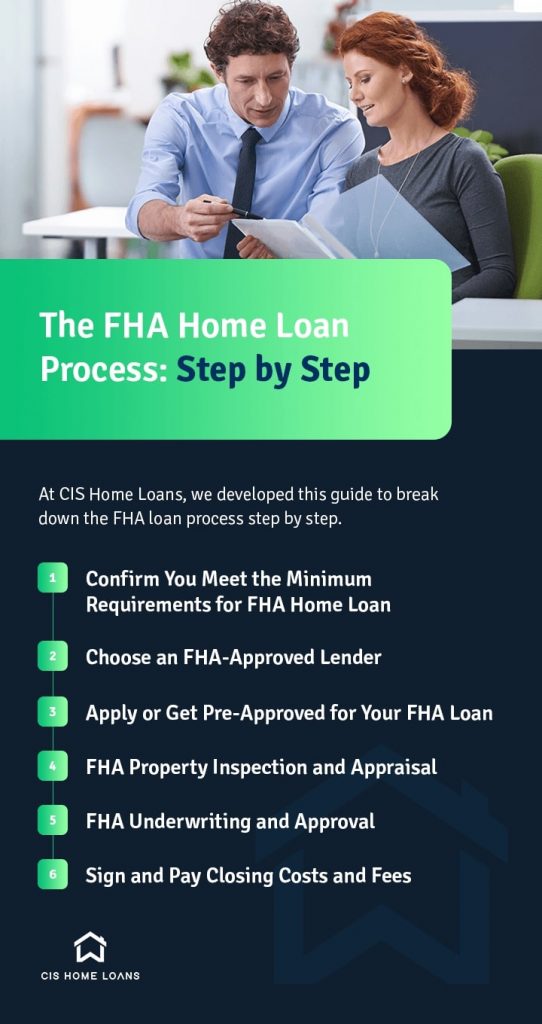

Understanding Mortgage Jargon: Key Terms Your Banker Hopes You Don't Ask About

When navigating the world of mortgages, understanding the jargon can save you both time and money. Many borrowers may feel overwhelmed by terms like amortization, escrow, and APR. Knowing what these terms mean will empower you to make informed decisions, especially when your banker throws these words around hoping you won't ask questions. To start, amortization refers to the gradual paying off of a loan over time through scheduled payments, while escrow involves a third-party account that temporarily holds funds during a transaction to ensure all conditions are met.

Furthermore, becoming familiar with points can greatly affect your mortgage costs. Points are fees paid directly to the lender at closing in exchange for a reduced interest rate, essentially a way to 'buy down' your rate. Understanding these strategies can lead to long-term savings. Additionally, terms like Loan-to-Value Ratio (LTV) signify how much of a property's value is financed through a mortgage; a lower LTV often results in better financing options. By grasping these crucial mortgage terms, you’ll be in a stronger position when discussing options with your lender.

Demystifying Home Loan Fees: What Your Banker Won't Tell You

When applying for a home loan, understanding home loan fees can feel like deciphering a foreign language. Your banker might gloss over many of these charges, leaving you with a hefty bill at closing. Common fees that often arise include origination fees, which are compensation for the lender's work in processing your application, and appraisal fees, which cover the cost of determining the market value of your home. It's crucial to read the fine print and ask questions about any fees you don't understand—after all, knowledge is power when making such a significant financial commitment.

Additionally, be aware of other hidden costs involved in the home loan process. Title insurance protects against claims against the property, while loan processing fees can cover the costs associated with ensuring your loan meets all legal requirements. You may also encounter document preparation fees for processing paperwork. To avoid surprises, ask your banker for a detailed breakdown of these charges before you sign anything. Remember, being informed will empower you to negotiate better terms and potentially save thousands over the life of your loan.

5 Questions to Ask Before Signing Your Home Loan Agreement

Before you commit to a home loan agreement, it's crucial to ask yourself some key questions that can save you from future financial stress. First, what is the total cost of the loan? This includes not just the principal and interest, but also any fees associated with the loan. Understanding the full cost upfront helps you budget more effectively and avoids surprises.

Another important question to consider is what is the interest rate? Is it fixed or variable? A fixed-rate mortgage offers stability, while a variable rate could change over time. Ensure you also inquire about the loan term, as the length of your agreement can significantly affect your monthly payments and overall cost.