Is Whole Life Insurance a Smart Investment or Just a Financial Burden?

When considering whether whole life insurance is a smart investment, it's crucial to weigh its benefits against its costs. Whole life insurance offers a guaranteed death benefit and a cash value component that grows over time, providing policyholders with a means of savings. This dual-purpose feature can be appealing for those looking to enhance their financial security while also preparing for the inevitable. However, it’s important to note that the premiums for whole life insurance are significantly higher than those of term life policies, which can lead some to view it as more of a financial burden than a viable investment option.

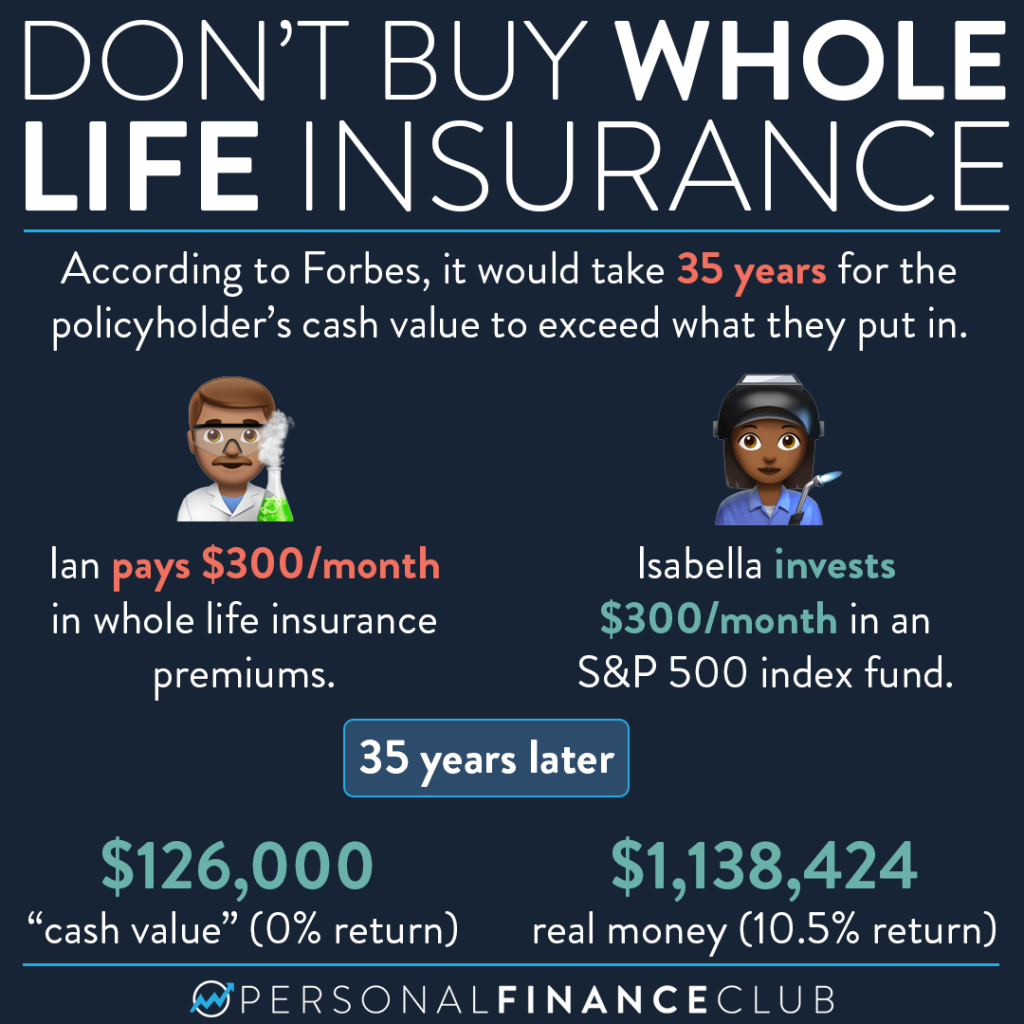

Furthermore, the debate on the effectiveness of whole life insurance as an investment continues, particularly in comparison to alternative investment vehicles. While whole life policies accumulate cash value, the growth rate is often modest compared to the potential returns from stocks or mutual funds. This leads many financial experts to recommend evaluating personal financial goals and seeking out diversified investment strategies instead. Ultimately, the choice of whole life insurance should align with individual circumstances, risk tolerance, and long-term objectives, ensuring that it serves as a tool for financial growth rather than a burden.

Understanding the Cash Value of Whole Life Insurance: What You Need to Know

Understanding the cash value of whole life insurance is essential for individuals considering this long-term financial commitment. Unlike term life insurance, which only provides a death benefit, whole life insurance builds cash value over time, acting as both a protective measure and a financial asset. The cash value increases at a guaranteed rate, providing policyholders not only with peace of mind but also with a growing investment that can be accessed during their lifetime. This dual purpose makes whole life insurance a unique solution for both protection and savings.

One crucial aspect to uncover is how the cash value of whole life insurance can be accessed. Policyholders can borrow against the cash value, take partial withdrawals, or even surrender the policy for its cash value, depending on their financial needs. However, it's important to remember that any outstanding loans or withdrawals will reduce the death benefit and overall cash value. Therefore, understanding the implications of accessing your cash value is key to making informed decisions about your policy.

Whole Life Insurance Explained: Benefits, Costs, and Common Misconceptions

Whole life insurance is a type of permanent life insurance that provides coverage for the insured's entire lifetime, as long as the premiums are paid. Unlike term life insurance, which expires after a set period, whole life policies build cash value over time, making them a versatile financial tool. The benefits of whole life insurance include lifelong coverage, a predictable premium payment schedule, and the ability to borrow against the cash value. Additionally, the death benefit is generally tax-free for beneficiaries, ensuring financial security for loved ones upon the policyholder’s passing.

Despite its advantages, there are common misconceptions about whole life insurance. Many individuals believe it is prohibitively expensive, failing to consider the lifelong benefits and cash accumulation that justify the higher premiums compared to term insurance. Others think that whole life policies are too complex to understand, when in fact, they can offer clear advantages for long-term financial planning. Understanding the costs associated with whole life insurance, including premiums and potential dividends, can help individuals make informed decisions that support their overall financial goals.